As a director of a limited company in the UK, you have flexibility in how you pay yourself. The most tax-efficient approach is often a blend of salary and dividends. In this blog, we will explore the optimum director’s salary for 2025/26, helping you stay tax-efficient while making the most of your Personal Allowance and avoiding unnecessary National Insurance contributions.

Why Take a Low Salary with Dividends?

Dividends are not subject to National Insurance. Pairing them with a modest salary helps you minimise your tax bill while keeping within legal limits. A small salary also ensures your company saves on Employer’s National Insurance. Plus, staying under the Personal Allowance means you avoid paying Income Tax altogether.

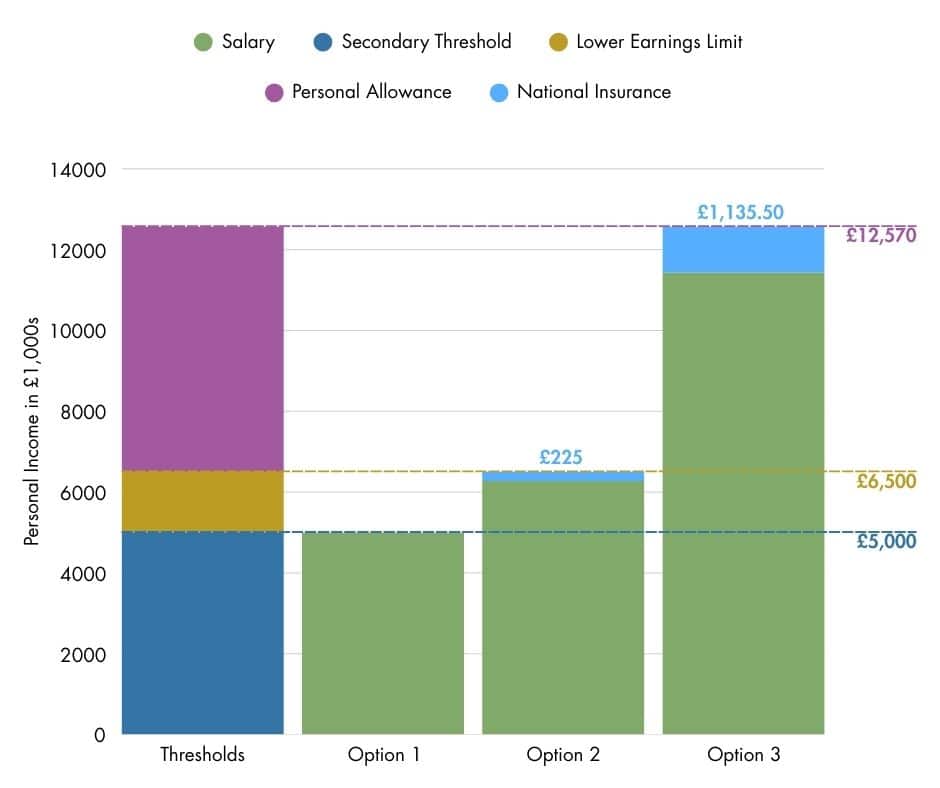

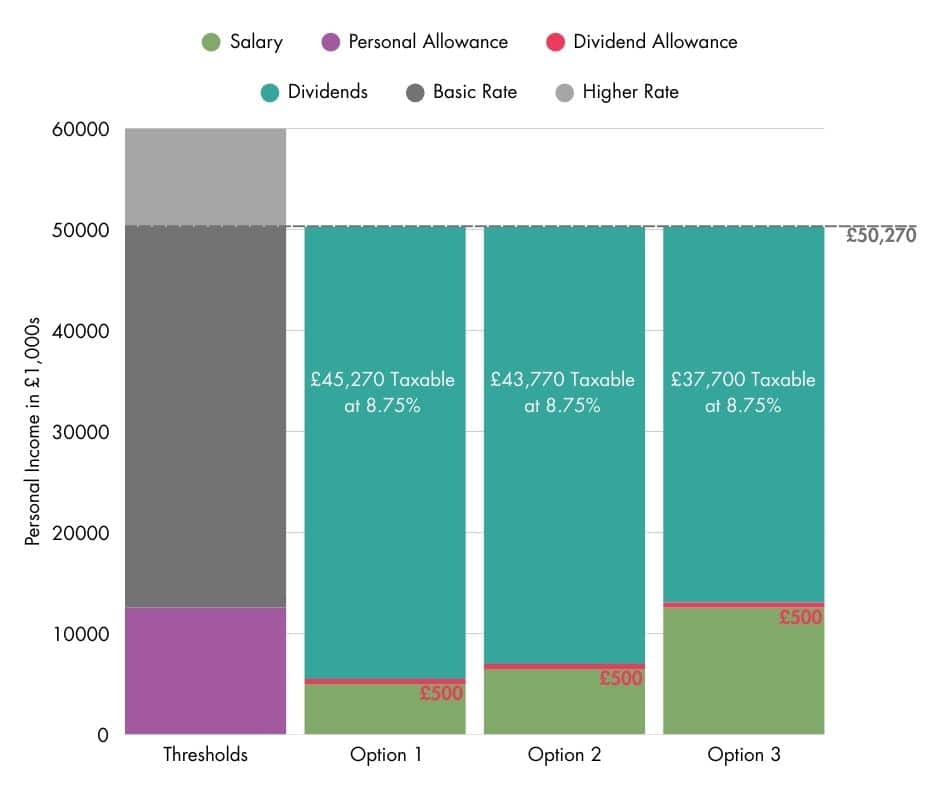

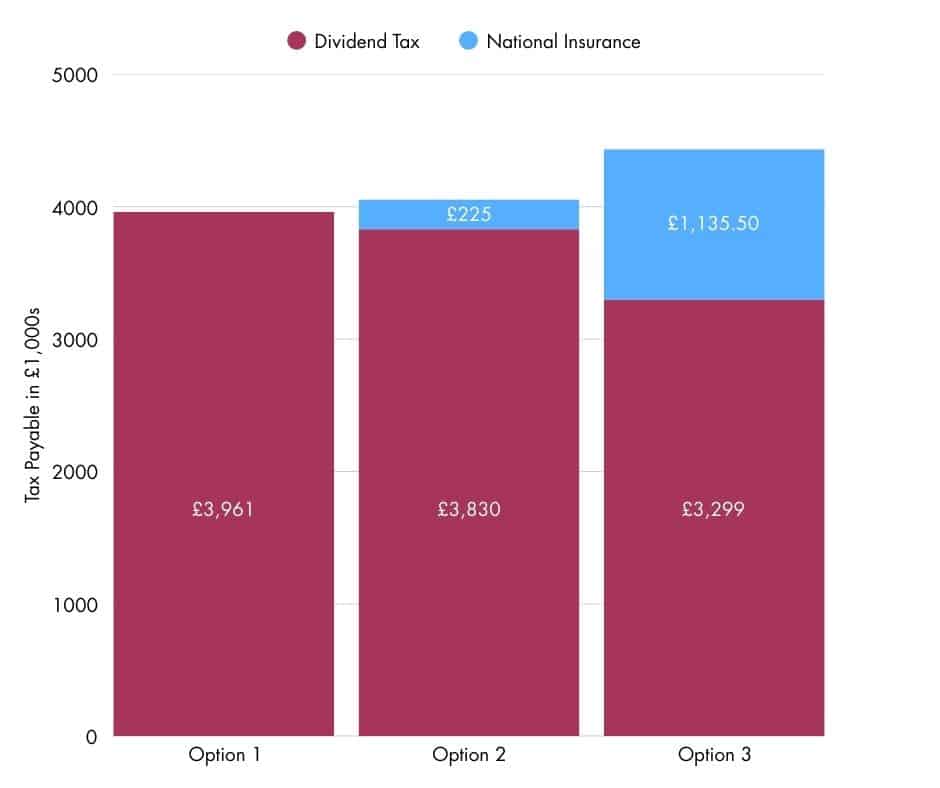

Optimum Director’s Salary for Sole Directors (2025/26)

| OPTION | ANNUAL SALARY | EMPLOYERS NI | QUALIFYING YEAR [1] | BEST FOR |

|---|---|---|---|---|

| 1 | £5,000 | £0 | No | Those who want zero payroll obligations [2] |

| 2 | £6,500 | £225 | Yes | Those who want low-cost access to pension and State benefits |

| 3 | £12,570 | £1,135.50 | Yes | Those looking to fully use their Personal Allowance [3] and reduce Corporation Tax |

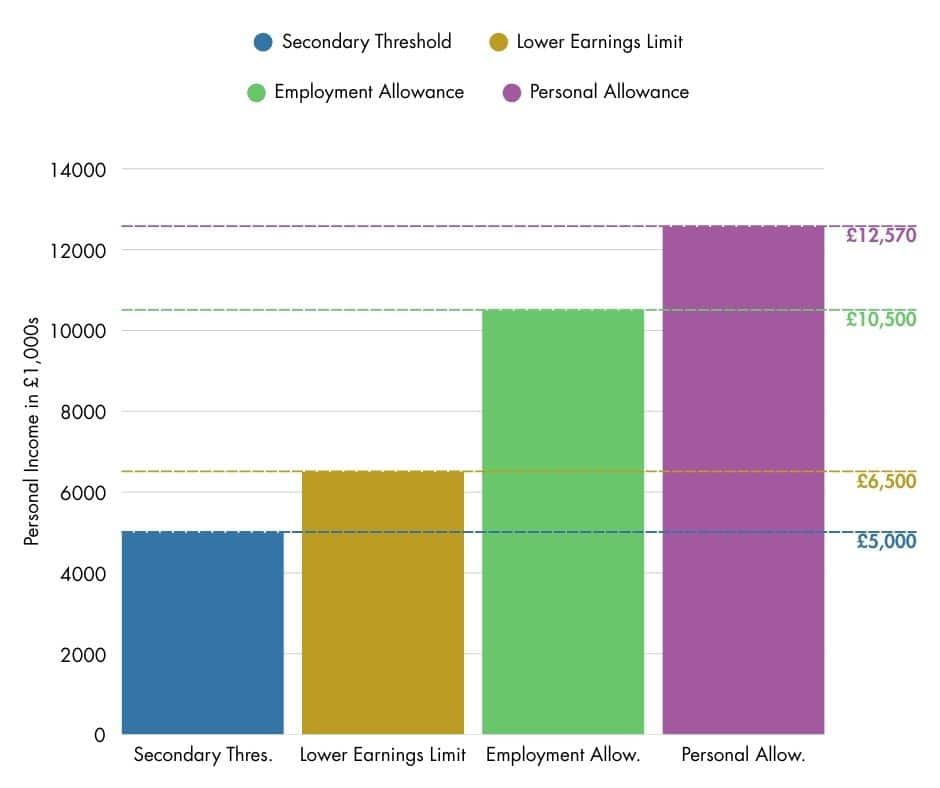

[1] To qualify for State Pension and other benefits, your salary must exceed the Lower Earnings Limit each year. This is £6,500 for 2025/26.

[2] You will avoid all tax, BUT you will not earn a qualifying year towards your State Pension.

[3] The Personal Allowance is the amount you can earn tax-free each year. This is £12,570 for 2025/26.

Optimum Director’s Salary for 2+ Directors or Employers (2025/26)

| OPTION | ANNUAL SALARY | EMPLOYERS NI (per director) [1] | QUALIFYING YEAR [2] | BEST FOR |

|---|---|---|---|---|

| 1 | £5,000 | £0 | No | Not Recommended as allowances are unused |

| 2 | £6,500 | £0 | Yes | Not Recommended as allowances are unused |

| 3 | £12,570 | £0 | Yes | Those looking to fully use their Personal Allowance [3] and Employment Allowance [1], while reducing Corporation Tax |

[1] Companies with 2+ directors or a sole director and 1+ employees may be eligible for the Employment Allowance, which will absorb a set amount of Employer NI each year (per company). This is £10,500 for 2025/26.

[2] To qualify for State Pension and other benefits, your salary must exceed the Lower Earnings Limit each year. This is £6,500 for 2025/26.

[3] The Personal Allowance is the amount you can earn tax-free each year. This is £12,570 for 2025/26.

What is the Employment Allowance?

The Employment Allowance allows eligible employers to reduce their Employer NI bill by up to £10,500. To qualify, your business must:

- Be registered as an employer

- Have at least 2 directors earning over the National Insurance threshold, or other employees

- Have had under £100,000 in Employer NI liabilities in the previous tax year

What Should You Do?

For sole directors, choose a mix that balances costs and benefits:

- £5,000 = No obligations but no State Pension credit

- £6,500 = Low-cost qualifying year

- £12,570 = Full Personal Allowance use and Corporation Tax reduction

For companies with 2+ directors or employers, the £12,570 salary is the clear winner. It leverages both the Employment Allowance and your Personal Allowance, resulting in zero National Insurance and tax liabilities.

Contact Us

We are not just accountants; we are Chartered Accountants with one of the most reputable and premium accounting bodies. We are registered and regulated by ACCA; so you can rest assured that you are in good hands. Knowing this, don’t hesitate to get in touch with us if you require assistance: Pi Accountancy | Contact Us

This article is for general informational purposes only and does not constitute legal or financial advice. While we aim to keep our content up to date and accurate, UK tax laws and regulations are subject to change. Please speak to an accountant or tax professional for advice tailored to your individual circumstances. Pi Accountancy accepts no responsibility for any issues arising from reliance on the information provided.